Central & Eastern Europe: the rising “promised land” for PE funds?

Who we areAbout usGeographic footprintCentral and Eastern Europe

CEE: the rising “promised land” for PE funds?

“Private capital isn’t just bouncing back, it’s powering Europe forward." (Eric de Montgolfier, CEO, Invest Europe): Private Equity in the CEE region is a growing, dynamic and maturing sector, increasingly drawing the attention of financial investors looking for market opportunities and promising returns.

Until lately, primarily centred on Poland, Czech Republic, Romania and Hungary which often served as primary regional hubs for the PE activity in CEE, the PE investments are now focusing increasingly on other parts of the region, notably the Adria Subregion.

Four main profiles of PE firms active in CEE

Analysing the Private Equity sector operating in CEE, four main types of PE funds can be identified:

- Large international PE funds, mainly from the U.S. and the U.K., focusing typically on large transactions with an Enterprise Value(EV) above €500 million;

- Pan-European PE funds, mainly coming from Western Europe (U.K., France, Germany), generally interested by mid-caps with an EV between €100-500 million;

- CEE-focused PE funds, most often headquartered in Warsaw, Prague, Vienna or in London, dealing with SMEs with €20-100 million EV;

- Purely local PE funds, active only in their country and targeting companies with €5-20 million of EV.

PE activity landscape revealing an increased interest for CEE

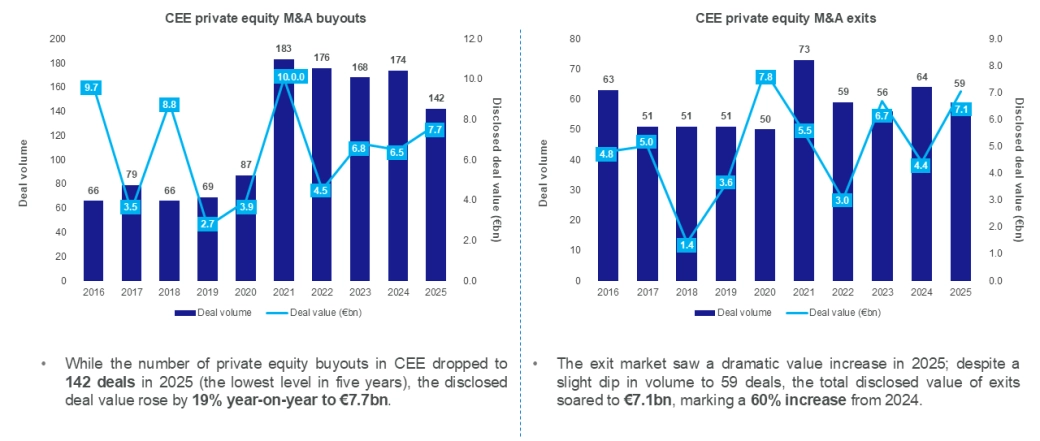

Based on Forvis Mazars’ “Investing in CEE: inbound M&A report 2025/2026” developed in collaboration with Mergermarket market intelligence, focusing on buyouts, the total value of all PE acquisitions announced in CEE in 2025 surpassed that of 2024, with €7.7bn worth of deals announced (+19% year-on-year) and a total of 142 buy-outs transactions (vs. 174 in 2024). The picture is similar with exits, where deals were fewer in number but considerably higher in value. In volume terms, 59 exits were announced in CEE, down 8% year-on-year, but the total value of these deals was €7.1bn – up 60% from 2024’s total.

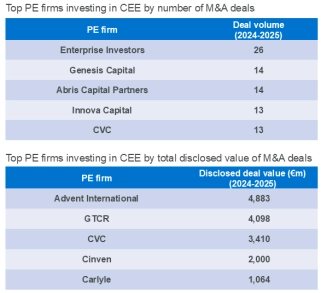

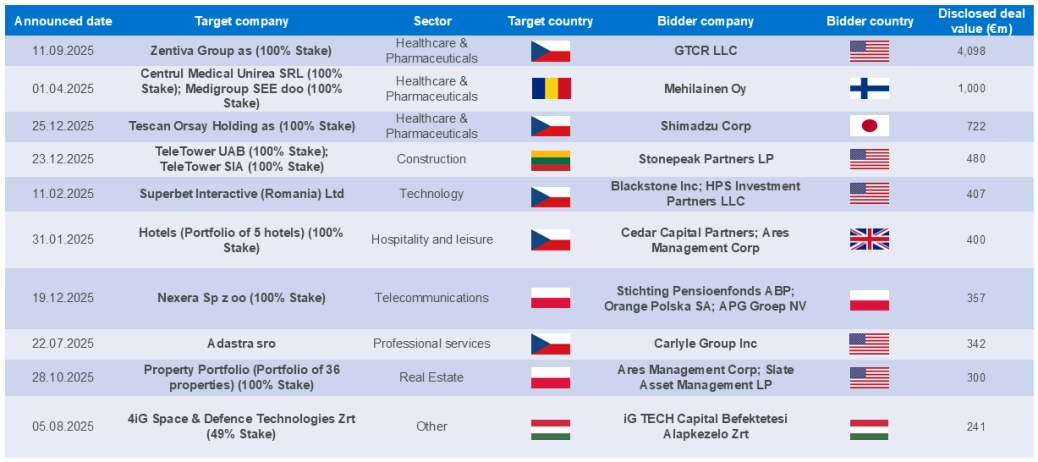

As far as the origin of PE funds investing in CEE during the last two years, four out of the five Regarding total disclosed value, all the top five PEs investing in CEE were leading international funds Out of the top 10 M&A deals realised in CEE last year, the vast majority involved a buyer coming from |

|

Private Equity in CEE: Top 10 PE M&A deals (2025)

Drivers that influence the CEE PE market

Several drivers are pushing the PE activity in Central & Eastern Europe. Among those:

- Relatively easy access to a large consumer market, with most CEE countries being part of the European Union and/or the Eurozone;

- Talent pool: CEE has a highly educated workforce, notably in engineering and IT, still being at a relatively lower costs than in Western Europe;

- Industrial nearshoring: with increase manufacturing and supply chain processes being relocated to CEE from Western Europe or Asia; EU funds often allow to have access to modern production facilities;

- Succession planning: with more than 70% of the companies owned by the first generation and founders, ownership transition is becoming a growing issue for a lot of firms. Options such as management buyouts (MBOs) are gaining popularity, where managers find a PE firm to secure a majority stake while retaining a minority share to keep "skin in the game".

- Relatively strong M&A activity and/or market consolidation in selected sectors, including manufacturing, energy & renewables, telecommunications, technology, healthcare & pharmaceuticals, consumer goods and defence.

Existing challenges and growth perspectives for 2026

The growth of PE investment activity in CEE stills faces a slower fundraising pace than in Western Europe. Relatively high valuation expectations from company owners might be a hurdle; many SMEs with strong fundamentals are waiting for better market valuations before committing to a sale. On the other hand, international investors might sometimes lack a local reach allowing to source deals in CEE, especially in the mid-segment.

While 2026 carries some political and economic challenges (geopolitical tensions worldwide, fiscal pressures, relatively high interest rates), the overall sentiment for the CEE region is one of “calculated optimism”. The CEE PE market is progressively growing, but still only accounts for less than 0.5% of regional GDP based on estimates, suggesting significant room for further penetration compared to Western Europe. Many global PE funds now view CEE as an attractive diversification play that will continue to offer higher development potential and lower entry multiples than the more mature markets. The expected Ukraine Reconstruction will also create interesting opportunities for the private equity ecosystem during the upcoming years.

For more information related to the Private Equity sector and/or CEE M&A market, download our 2026 Global Private Equity Report and/or our Investing in CEE: inbound M&A report 2025/2026

Want to know more?

Pere Mioč Partner, Tax Advisory - Zagreb, Croatia